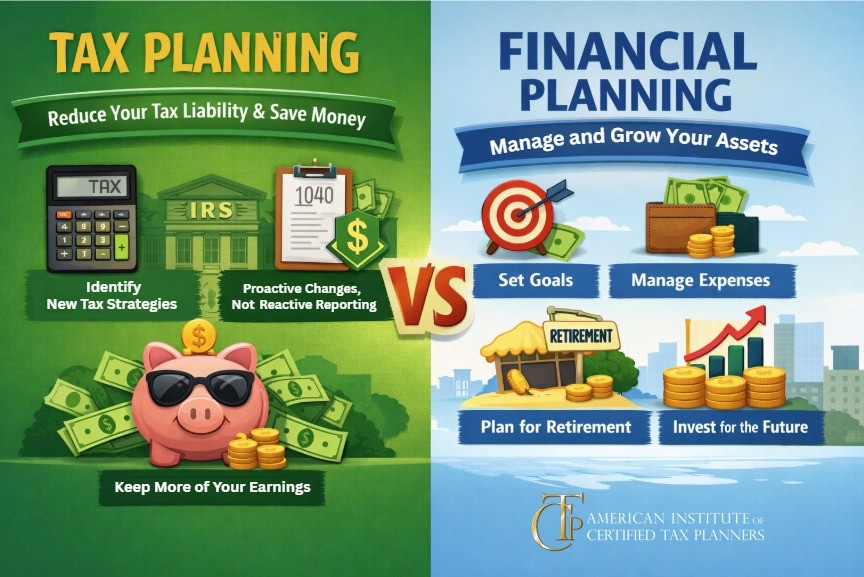

Tax Planning vs. Financial Planning: Why You Need to Understand the Difference

Many business owners assume tax planning is something to think about later – often lumped together with retirement or viewed as a byproduct of financial

TAX PLANNING 101: Busting the Myth that Tax Planning is Only for the Rich! Part 1

By now, everyone has figured out that America’s wealthy and elite are not always avoiding taxes through illegal means. There are thousands of court-tested, law-abiding

TAX PLANNING 101: Ideas for Reducing Taxable Income and Maximizing Tax Credits Part 2

We are continuing to bust the myth that significant tax savings are only applicable to the rich and wealthy. Countless moderate-income earners are utilizing the

Business debt restructuring: How to do it with money saved on taxes

It’s common practice for businesses to take on debt, but unforeseen occurrences like a recession or a pandemic might make it more challenging to make

How your clients can reduce their children’s taxes and get out of debt with the money saved

Taxes can be stressful. The last thing your clients, who probably wear multiple hats, want to do is send more of their hard-earned money to

How Joint Ventures Can Dramatically Grow Your Tax Planning Business

For tax professionals in particular, one pro tip has the potential to alleviate stress and accelerate your business growth: that is to start a joint

Tax Planning Software – Artificial Intelligence or Skill Saw?

By Dominique Molina, CPA MST CTS Have you asked yourself, do I really have to study tax planning? Can’t I just select a software providing

Tax Strategies for Selling an S Corporation: Failing the §302 Stock Sale Tests

As a tax planner, when a client approaches you about selling their S corporation, one of the first questions to ask is whether they are

Tax Strategies for Selling an S Corporation: Planning for an Asset Sale

Even if you have never assisted a client with the sale of a business, as a tax planner you have the potential to provide tremendous

How Partnering with Technical Experts Makes It Easier to Offer Services to Your Clients

Brought to you by Tri-Merit High-performing accounting firms focus on providing high-value, specialized services tailored to their clients’ needs. If you are offering tax planning, that

Ethical Considerations for Tax Professionals: Standards and Penalties for Tax Positions

When tax professionals prepare a tax return, they are typically aiming for the return to be correct “beyond a reasonable doubt.” However, this is hardly