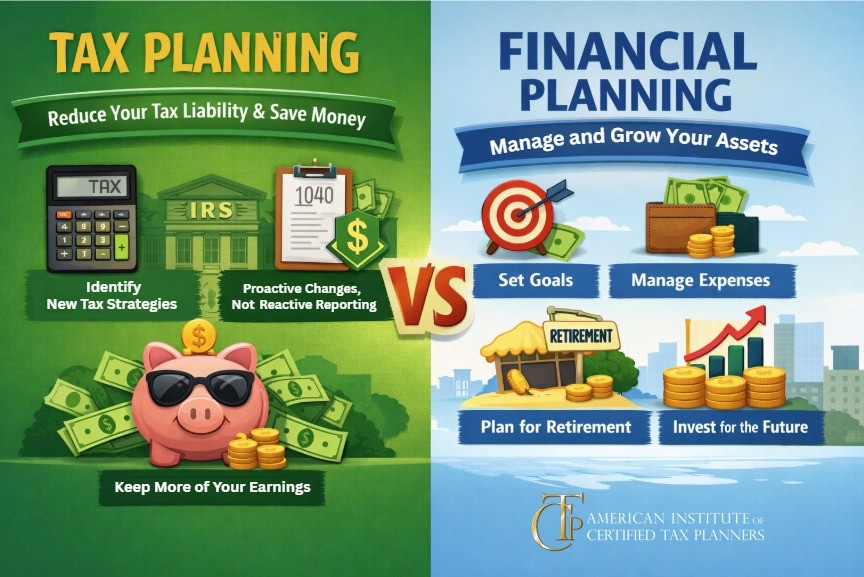

Tax Planning vs. Financial Planning: Why You Need to Understand the Difference

Many business owners assume tax planning is something to think about later – often lumped together with retirement or viewed as a byproduct of financial

Tax Strategies for Investments: Securing the 0% Capital Gains Tax Rate

First-time investors may spend a great deal of time and effort researching the best possible investment opportunities—but fail to take into consideration the tax consequences.

Tax Strategies for Investments: Making Use of Loss Harvesting and Loss Carryovers

Profiting from investments and reducing tax liability may seem like competing goals, but both can be accomplished with a little proactive tax planning. In the

Tax Strategies for Investments: Controlling Timing for Capital Gains

Long-term investment success is about more than the initial investment decision. As tax professionals know, timing can have a dramatic impact on the tax consequences

Section 174 and R&E – Uncertainty and Questions

By Kevin Zolriasatain, Principal of KBKG Many businesses, small and large, rely on research and development to improve their offerings, compete with international markets, and

Oil and Gas: Where is the opportunity?

By Chase Ravsten, Vice President of Vistia Capital Investing in oil and gas can offer potential advantages: Oil and gas are still a staple of

Tax Deductions for Business Vehicles: Using Standard Mileage vs Actual Expenses

New business owners may be excited to learn that the IRS also allows them to deduct their annual business mileage as a business expense. However,

Tax Deductions for Business Vehicles: Section 179 vs. Bonus Depreciation

When it comes to vehicle tax deductions, tax planners face a number of challenges—from keeping up with recent changes to the tax rules to educating

Accounting Pricing Strategy

Accounting Pricing Strategy One of the most difficult, yet important, issues you must decide as tax business owner is how much to charge for your

Limiting the Substance Over Form Doctrine

At the end of 2018, to the dismay of the IRS and the Tax Court, the Second Circuit joined the First and Sixth in reversing

Conservation Easements Make the IRS Dirty Dozen Tax Scam List

The IRS has put conservation easements on its annual “Dirty Dozen” list which, says the IRS, “represents the worst of the worst tax scams.” The